GST Registration Limit: 20 Lakh or 40 Lakh? Plus Documents & Why It's Required

The 20 vs 40 lakh GST threshold explained - which applies to your business, what documents you need to file, and why GST registration is legally required above the limit.

- The 20 vs 40 lakh GST threshold explained - which applies to your business, what documents you need to file, and why GST registration is legally required above the limit.

- Use this as a gst basics checklist for gst registration limit, not as a substitute for checking current official or platform rules.

- Confirm thresholds, filing dates, forms, documents, and portal guidance against the source links before filing, buying software, changing campaigns, or changing a workflow.

India has over 63 million MSMEs (Ministry of MSME, 2024) - but only 1.51 crore active GST registrations (PIB, April 2025). That gap exists partly because millions of small businesses don't know which threshold applies to them, what documents they need, or why registration is legally required. This post answers all three.

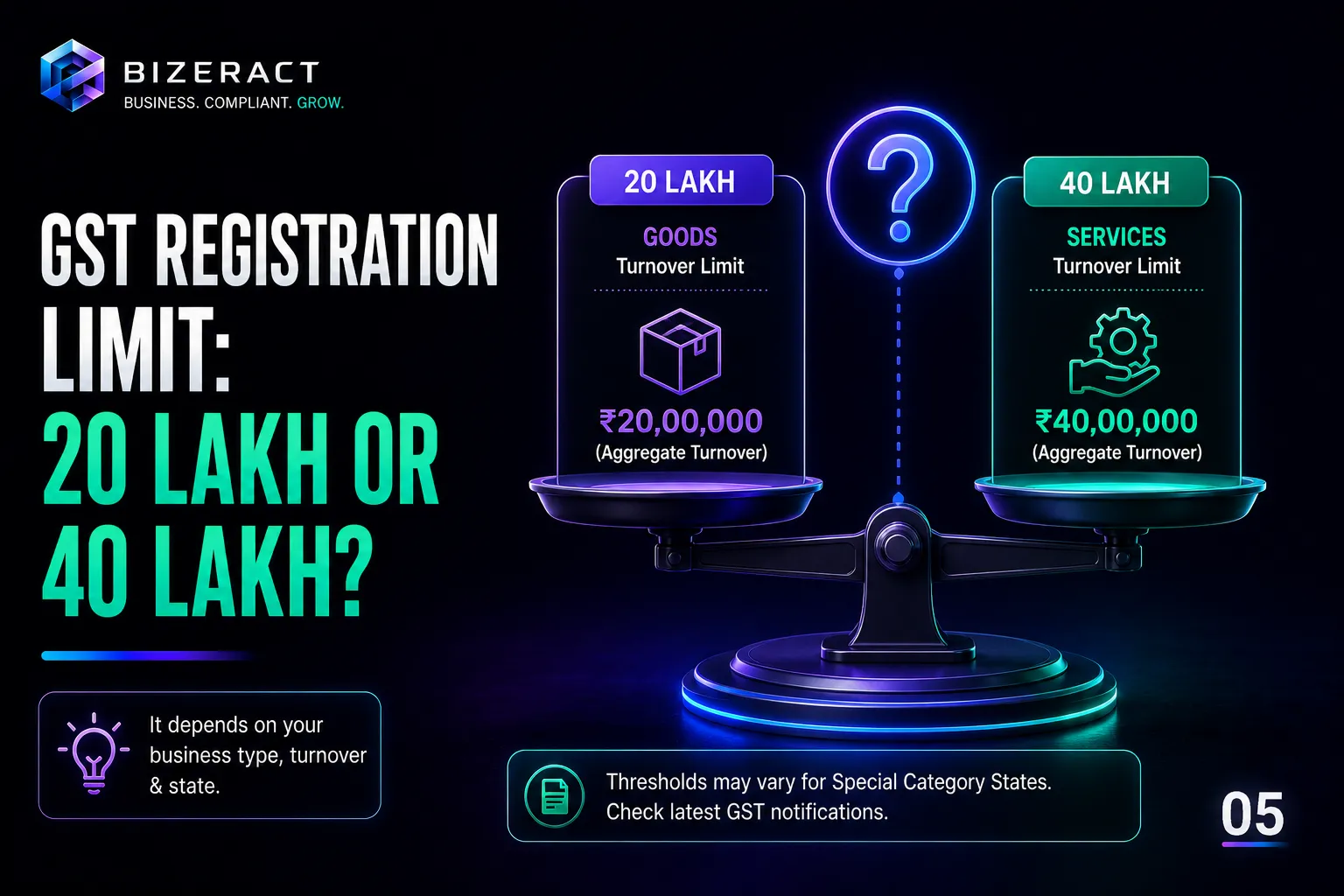

- The ₹40 lakh threshold applies only to pure goods suppliers in most states - introduced April 1, 2019.

- Services businesses and mixed suppliers: ₹20 lakh threshold still applies (retained from 2017).

- GST now contributes approximately 27.9% of India's total tax revenue - ₹22.08 lakh crore in FY 2024-25 (PIB, 2025).

- 1.50 crore informal micro enterprises registered on Udyam Assist Platform still operate without a GSTIN (PIB, 2024).

- Documents required differ by entity type - proprietorships need 5 documents; companies need 7+ including DSC.

Is the GST registration limit 20 lakhs or 40 lakhs?

Both figures are correct - they apply to different business types. The GST Council introduced the ₹40 lakh threshold on April 1, 2019 (PIB notification, March 7, 2019) specifically for suppliers of goods in most Indian states. The original ₹20 lakh threshold from 2017 remains in force for service providers and businesses making mixed supplies.

| Business type | Most states threshold | Special category states* |

|---|---|---|

| Pure goods supplier | ₹40 lakh/year | ₹20 lakh/year |

| Service provider | ₹20 lakh/year | ₹10 lakh/year |

| Mixed goods + services | ₹20 lakh/year | ₹10 lakh/year |

*Special category states with lower thresholds: Manipur, Mizoram, Nagaland, Tripura, and Union Territories of J&K, Himachal Pradesh, and Uttarakhand opted for the ₹20 lakh goods threshold instead of ₹40 lakh.

The trap that catches most business owners: if you sell goods and also charge for any service - delivery, installation, warranty, consulting - you're classified as a mixed supplier. Your entire aggregate turnover then falls under the ₹20 lakh limit, not ₹40 lakh. A furniture shop doing ₹38 lakh in sales but also charging ₹2 lakh for installation services crossed the ₹20 lakh limit long before they crossed ₹40 lakh.

Why is GST registration required by law?

GST now accounts for approximately 27.9% of India's total tax revenue - ₹22.08 lakh crore collected in FY 2024-25 alone, growing 9.4% year-on-year (PIB, 2025). That scale is only possible because registration is mandatory, not optional, above the threshold. Section 22 of the CGST Act makes it a legal obligation.

Beyond legal compliance, the practical reasons registration matters for your business:

- Tax invoice rights. Only registered businesses can issue a valid tax invoice. Without one, your B2B buyers can't claim Input Tax Credit - so they simply won't purchase from you.

- Inter-state sales unlock. Any sale that crosses a state border requires GST registration, regardless of turnover. A Mumbai manufacturer selling to a Bengaluru buyer triggers mandatory registration from the first invoice.

- E-commerce access. Amazon India, Flipkart, Meesho, and every major Indian marketplace require GSTIN before your first listing - with no turnover threshold exemption.

- ITC on your own purchases. Registered businesses reclaim GST paid on inputs. Unregistered businesses absorb it as a cost - effectively paying 18% more for every business expense.

- Penalty avoidance. Operating above-threshold without registering: minimum ₹10,000 penalty or 10% of tax due under Section 122, CGST Act.

What documents are required for GST registration?

Document requirements vary by business structure. CBIC issued new guidelines in April 2025 (Instruction 03/2025-GST) to streamline document standards and reduce rejection rates. Here's the current checklist:

| Document | Proprietorship | Partnership / LLP | Pvt Ltd / OPC |

|---|---|---|---|

| PAN | Proprietor's personal PAN | Firm PAN | Company PAN |

| Aadhaar | Proprietor's (active mobile linked) | Authorised partner | Authorised director |

| Address proof | Electricity bill <3 months + rent agreement or NOC if rented | Same | Same |

| Bank document | Cancelled cheque or statement with IFSC printed | Same | Same |

| Photo | Proprietor passport-size | All partners | All directors |

| Constitution proof | Not required | Partnership deed | MOA + AOA + incorporation certificate |

| DSC | Not required | Required for LLP | Required for all directors |

The most common rejection reason is an address proof in the landlord's name without an NOC letter. If the electricity bill is in your landlord's name, you need both the bill and a signed NOC from the property owner on plain paper - without it, the officer will raise a Show Cause Notice.

Can a normal person apply - or do you need a company?

Any Indian individual with a PAN and an active Aadhaar-linked mobile number can apply for GST registration. A home address works as the principal place of business for proprietorships - there's no requirement for a separate commercial office.

Notably, 1.50 crore informal micro enterprises registered on the Udyam Assist Platform within 14 months of its launch (PIB, 2024) - demonstrating that sole proprietors and micro-businesses are registering in large numbers, even at very small scale. The barrier isn't eligibility; it's usually document readiness and threshold confusion.

What happens if you miss the registration window?

Once you become liable (threshold crossed, or inter-state sale made), you have 30 days to apply. After that window, the penalty clock starts. You owe GST retroactively from the date you became liable - plus the Section 122 penalty minimum of ₹10,000. Buyers who transacted with you during the unregistered period also lose their ITC claims, which creates a secondary commercial dispute on top of the tax liability.

Frequently asked questions

Is the ₹40 lakh threshold applicable for all states?

No. Manipur, Mizoram, Nagaland, Tripura, and certain Union Territories opted for the ₹20 lakh goods threshold instead of ₹40 lakh. Service providers in all states retain the ₹20 lakh limit regardless. Always check the specific notification for your state if you're near the boundary.

Does the threshold reset every year?

Yes. Aggregate turnover is calculated on a financial year basis (April–March). If your turnover crosses the threshold mid-year, you must register within 30 days of crossing it. In the following year, if turnover stays below the threshold, you can apply for voluntary cancellation - but the registration remains mandatory for the year it was crossed.

Why is GST registration required even for small businesses selling online?

Section 24(ix) of the CGST Act mandates GST registration for all persons supplying goods or services through e-commerce platforms that collect TCS, regardless of turnover. Amazon, Flipkart, and Meesho all collect TCS - so their sellers must register before their first sale. This rule applies even if your annual turnover would be below the ₹20 lakh or ₹40 lakh threshold.

Ready to file? Our online GST registration service delivers your GSTIN in 24 hours - documents to certificate, ₹499 flat. Also see: full GST registration overview for all entity types and GST for small businesses for a threshold calculator and composition scheme comparison.

What should you verify before using this GST Basics guide?

Before acting on gst registration limit, verify the current rules or platform behavior with the GST Portal. The practical answer depends on your business model, state, turnover, documents, software stack, and whether the decision affects tax, customer data, paid media spend, or a production workflow.

Use this article as a working checklist, then confirm thresholds, registration status, return forms, document rules, and portal notices. In our audits, most expensive mistakes do not come from ignoring the whole process. They come from one stale assumption, one mismatched address, one missing event, or one automation path that nobody tested after launch.

| Checkpoint | Why it matters | Where to confirm |

|---|---|---|

| Current rule or platform status | Limits, forms, policies, and APIs can change after a blog update. | GST Portal |

| Your exact business case | A local shop, freelancer, D2C store, agency, and SaaS team rarely need the same next step. | Documents, invoices, campaign data, analytics setup, or workflow logs |

| Implementation evidence | The safest GST decision is backed by proof, not memory or screenshots from an old setup. | Portal acknowledgement, dashboard export, invoice sample, test lead, or error log |

How do we apply this in real business work?

We start with the smallest decision that can be verified. For compliance work, that means matching PAN, address, bank, invoices, and portal status before filing. For websites, marketing, analytics, and automation, it means testing the real user path from first click to final record. The boring checks catch the costly failures.

A useful rule: if a claim changes money, tax, reporting, or customer communication, keep evidence for it. Save the acknowledgement, export the report, test the form, and note the date you verified the source. That gives you a clean trail when a client, officer, platform, or internal team asks why the setup was done that way.

When should you get expert review?

Get expert review when the next action can create tax exposure, lost reporting data, ad waste, broken customer communication, or production downtime. A simple self-check is enough for low-risk learning. A filed return, new registration, tracking migration, paid campaign restructure, or live automation deserves a second set of eyes before it affects customers or records.

How often should this be rechecked?

Recheck the decision whenever your turnover, state, product mix, campaign budget, website stack, analytics property, or workflow ownership changes. Also recheck it after major portal updates, platform policy changes, annual filing deadlines, and vendor migrations. The guide is useful today only if the facts behind it still match your business.

What is the fastest safe way to decide?

Write the decision in one sentence, list the proof needed for that sentence, and verify only those items first. This keeps the work focused. If the proof confirms the decision, proceed. If one item is unclear, pause and resolve that point before changing filings, campaigns, tracking, website code, or automation logic.

What can go wrong if you skip verification?

The usual failure is not dramatic at first. It looks like a rejected application, a wrong tax invoice, a missing conversion, a duplicate lead, a broken report, or a workflow that silently stops. Those small failures become expensive when nobody notices them until month-end reporting, filing day, or a customer escalation.

What evidence should you keep after making the change?

Keep enough evidence to reconstruct the decision later. For a compliance topic, that usually means the application reference number, registration certificate, invoice sample, return acknowledgement, payment challan, notice reply, or source link checked on the day of filing. For a website, campaign, analytics setup, or automation, keep the before-and-after screenshot, test submission, dashboard export, webhook log, and the exact setting that changed.

This matters because most business fixes are revisited months later, when nobody remembers the original reason. A short evidence trail makes audits faster, handovers cleaner, and vendor conversations more precise. It also keeps the advice in this guide tied to your real operating context instead of becoming a generic checklist that gets copied without review.

- Date checked: record when the official source, dashboard, or portal screen was reviewed.

- Business context: note the entity, state, product, campaign, property, or workflow affected.

- Proof of action: save the acknowledgement, report export, test result, or live URL.

- Owner: assign one person to re-check the item when rules, tools, or business volume change.

Which next step should you take after reading this?

Turn the article into one action list. Mark what is already true, what needs proof, and what needs expert review. If you want to go deeper, compare this guide with GST Registration, GST Registration for Small Business, and GST Registration Online India. Then update the decision only after the official source and your own records agree.

Frequently asked questions

What is the short answer on GST Registration Limit?

The 20 vs 40 lakh GST threshold explained - which applies to your business, what documents you need to file, and why GST registration is legally required above the limit. The practical next step is to compare the article checklist with your business model, state, turnover, documents, and tools before you act.

What should I verify before using this guide?

Verify the latest thresholds, filing dates, forms, documents, and portal guidance from the official source links on this page. Tax rules, ad platform policies, software APIs, marketplace requirements, and search documentation can change after publication.

When should I get professional help?

Get help when the decision affects GST registration, tax filing, paid media budget, production website performance, analytics accuracy, or business-critical automations. A short expert review usually costs less than penalties, rework, bad data, or failed implementation.

Let's talk about your business.

Tell us what you're working on and where you want to go. We'll put together a plan. No obligation, no sales pitch.

- Free 30-minute call

- A plan built around your goals

- No obligation, no pressure

- Your own account manager